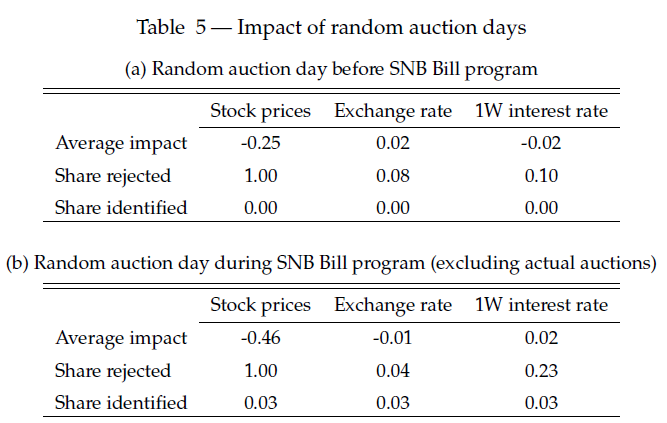

class: center, middle, inverse, title-slide # Shocking Interest Rate Floors ### Fabio Canetg</br>Uni Bern ### Daniel Kaufmann</br>Uni Neuchâtel and KOF Swiss Economic Institute ### SNB Research Seminar, Zurich 18 October 2019 --- class: general # Introduction - Central banks in advanced economies strongly expanded the monetary base through large-scale asset purchases and foreign exchange interventions - Therefore, money market rates hit an interest rate floor ("effective lower bound"; zero; deposit rate; interest paid on reserves) -- - Several ways to raise the money market rate: + Sell assets + Pay higher interest on reserves + Issue term deposits + Offer reverse repo's + **Issue interest-bearing central bank debt securities** --- class: general # Volume of SNB Bills and reserves The Swiss National Bank issued **SNB Bills** to drain reserves (sight deposits) .image-center[  ] --- class: general # What we do and find **Research question:** What is the effect of central bank debt? - **Theory:** In a partial equilibrium money market model + the money market rate increases with the volume of, and yield on, central bank debt + central bank debt determines an interest rate floor, similar as interest on reserves -- - **Empirics:** Causal identification of two orthogonal shocks through heteroskedasticity and local projections + Shock 1 explains 68% of variation in money market rate; has modest effects on other variables; resembles money market model + Shock 2 appreciates the Swiss franc, lowers stock prices, lowers long-term interest rates, and increases corporate bond risk premia; suggests strong effects through changes in expectations (e.g. Bäurle/Kaufmann, 2018) --- class: general # Related literature **Exit strategies with large excess reserve balances:** - Interest on reserves (e.g. Goodfriend, 2002, Keister et al., 2008) - Central bank debt and other tools (Berentsen et al., 2018) - Empirical evidence scarce; impact debated (Selgin, 2018, Hendrickson, 2018, Ireland, 2014) -- **The effects of monetary policy:** - Multiple dimensions of official decisions. Different effects of target changes, forward guidance, and QE (Gürkanyak et al., 2005, Gürkaynak/Wright, 2012, Swanson, 2017, Altavilla et al., 2019) - QE signalling channel (Woodford, 2012, Bauer/Rudebusch, 2014) - Information channel (Nakamura/Steinsson, 2018, Jarocinski/Karadi, 2018, Altavilla et al., 2019) - Temporary vs. permanent effects of QE (Wright, 2012, Swanson, 2017) --- class: general # Related literature **Dynamic event studies:** - Identification through heteroskedasticity (Rigobon, 2003) - Identification impulse responses through heteroskedasticity with VAR (Wright, 2012) - High-frequency identification with local projections (Swanson, 2017) - Recover dimensions of high-frequency shocks by factor rotations (Swanson, 2017, Altavilla et al., 2019) --- class: outline # Outline 1. A model of the money market 2. Empirical strategy 3. Empirical results 4. Concluding remarks --- class: inverse, center, middle # 1. A model of the money market --- class: general # Timing and features of the model 1. Banks hold an exogenous amount of reserves `\(F\)` ("pre-auction reserves") and have to fulfill a reserve requirement `\(K\)` at the end of the day -- 2. Central bank allows banks to invest a share `\(\pi^{cb}\)` of their pre-auction reserves in debt securities with a pre-determined yield `\(i_b\)`. Debt securities do not count towards reserve requirements. Banks commit to how much they actually invest `\(\pi\)` -- 3. They can borrow (or lend) reserves `\(B\)` on the money market to finance the debt securities, or to fulfil reserve requirements `\(K\)` at the end of the day -- 4. Banks are prone to a random liquidity shock `\(Z\)`, and potentially face a liquidity shortage if `\(z > (1-\pi)F-K\)` . The probability of a liquidity shortage amounts to `$$P(X>0),\ \ X = Z + K - (1-\pi)F$$` -- 5. In case of a liquidity shortage, banks have to borrow at the higher discount rate `\(i_x\)` --- class: general # Optimal behaviour of banks Optimal behavior requries that the expected marginal benefit of borrowing on the money market equals expected marginal cost. - **Marginal benefit** + a larger buffer in case of a liquidity shortage `\((1-\pi)i_x P(X>0)\)` + a higher interest income from debt securities `\(\pi i_b\)` - **Marginal cost** + the money market rate `\(i_m\)` -- **Alternative intuition:** Lending an additional unit on the money market should yield the same return as investing `\(\pi\)` in debt securities `\((\pi i_b)\)` plus a "risk premium" because the liquidity buffer declines by `\((1-\pi)\)` --- class: general # Equilibrium money market rate > **Proposition 1:** *If each commercial bank maximizes expected profits with respect to* `\(B_i\)` *and* `\(\pi_i\)`*, the money market rate equals* > `$$i_m = i_b\pi + (1-\pi) i_xP(X>0)$$` - With `\(\pi = 0\)` this is the model of Poole (1968) -- - In our model, the money market rate is affected by the volume of, and yield on, debt securities -- - With ample reserves `\(F\rightarrow \infty\)` the probability of a liquidity shortage is zero `\(P(X>0)\rightarrow 0\)`, and the money market rate approaches the interest rate floor `\(i_m = \pi i_b\)` -- > **Key insight:** For a strictly positive `\(i_b\)`, issuing central bank debt determines an interest rate floor, similar as interest on reserves --- class: general # Illustration with calibrated model .image-center-wide[ ] Left panel: money demand curves conditional on `\(i_b=0.10\%\)`. Right panel: money demand curves conditional on `\(\pi^{cb}=0.5\)`. --- class: general # SNB Bills and money market rates .image-center[  ] `\(i_m = i_b\pi = 0.22\%\times78\% =0.17\%\)`, close to, but above, SAR 3M `\((0.091\%)\)` at end of sample --- class: inverse, center, middle # 2. Empirical strategy --- class: general # The timing of auctions was deterministic The auctions were announced in advance, almost always weekly, usually on the same day of the week .image-center[  ] --- class: general # Model Suppose stock prices `\((s_t)\)` and interest rates `\((r_t)\)` are generated by *three* i.i.d. structural shocks `\((e_{1t}, e_{2t}, e_{3t})\)`, with variance 1, where `\(\psi_{ij}\)` denotes the immediate impact of shock `\(j\)` on variable `\(i\)` -- **Deterministic timing of auctions:** Shocks 1 and 2 occur only on SNB Bill auction days. All other shocks (shock 3) occur on all days: `$$s_{t} = \begin{cases} {\psi_{s1}e_{1t}+\psi_{s2}e_{2t}+\psi_{s3}e_{3t}} & \text{for}\ t \in \{\text{auction}\}\\ {\psi_{s3}e_{3t}} & \text{for}\ t \in \{\text{no auction}\}\\ \end{cases}$$` `$$r_{t} = \begin{cases} {\psi_{r1}e_{1t}+\psi_{r2}e_{2t}+\psi_{r3}e_{3t}} & \text{for}\ t \in \{\text{auction}\}\\ {\psi_{r3}e_{3t}} & \text{for}\ t \in \{\text{no auction}\}\\ \end{cases}$$` -- We control for other shocks by computing the difference of the variance-covariance matrix between auction days and non-auction days: `$$\Omega_{t\in A} - \Omega_{t\not \in A} = \left[\begin{array}{cc} \color{red}{\psi_{s1}^2+\psi_{s2}^2}+\color{blue}{\psi_{s3}^2} & \color{red}{\psi_{s1}\psi_{r1}+\psi_{s2}\psi_{r2}}+\color{blue}{\psi_{s3}\psi_{r3}} \\ . & \color{red}{\psi_{r1}^2+\psi_{r2}^2}+\color{blue}{\psi_{r3}^2} \end{array}\right]-\left[\begin{array}{cc}\color{blue}{\psi_{s3}^2} & \color{blue}{\psi_{s3}\psi_{r3}} \\ . &\color{blue}{\psi_{r3}^2} \end{array}\right]$$` --- class: general # Recovering two orthogonal dimensions - "Money market rate shock" (shock 1) + Money market rate increases - "Expectation shock" (shock 2) + Does not affect the money market rate + Lowers stock prices -- `$$\Omega_{t\in A} - \Omega_{t\not \in A} =\left[\begin{array}{cc} \psi_{s1}^2+\psi_{s2}^2 & \psi_{s1}\psi_{r1}+\color{red}{\underbrace{\psi_{s2}\psi_{r2}}_{0}} \\ . & \psi_{r1}^2+\color{red}{\underbrace{\psi_{r2}^2}_{0}} \end{array}\right]=\left[\begin{array}{cc} \omega_{11} & \omega_{12} \\ . & \omega_{22} \end{array}\right]$$` -- `$$\psi_{r1} = \color{red}{+}\sqrt{\omega_{22}}, \ \ \ \ \ \ \ \ \ \psi_{s1} = \omega_{12}/\psi_{r1}, \ \ \ \ \ \ \ \ \ \ \psi_{s2} = \color{red}{-}\sqrt{\omega_{11}-\psi_{s1}^2}$$` --- class: general # Dynamic effects and variance decomposition - The responses are scaled to a one-standard deviation shock - To assess their overall importance, we can compute `$$\text{Var. decomposition}_{ij} = \frac{\psi_{ij}^2}{\Omega_{t\in A, ii}}$$` -- - We can estimate dynamic effects and control for potential persistence in the variables, calculating the variance-covariance matrices on auction and non-auction days using the difference in forecast errors from local projections `$$\begin{eqnarray}\nonumber \mathbb{E}[y_t|y_{t-1} ]-\mathbb{E}[y_t|y_{t-2} ] &=&\mathbb{E}[y_t|y_{t-1} ]-y_t-\mathbb{E}[y_t|y_{t-2} ]+y_t\\\nonumber &=& \varepsilon_{t|t-2} - \varepsilon_{t|t-1} \\\nonumber &=& \Psi_0e_{t}+\Psi_1e_{t-1}-\Psi_0e_{t} = \Psi_1e_{t-1} \end{eqnarray}$$` - **Intuition:** If a forecaster revises its forecast more strongly on an SNB Bill auction day than on other days, this tells us something about its the causal effect --- class: general # Data and estimation **Sample:** 20 October 2008 to 28 July 2011 **For identification:** - SNB Bill auction days (and other monetary/fiscal operations) - Sign and zero restrictions on one-week zero coupon yield from interest rate swaps - Sign restriction on Swiss Market index -- **Domestic variables:** Nominal effective exchange rate, money market rates, government bond yields, corporate bond yields, various spreads **Foreign variables:** EUR/USD, Euro Stoxx 50, 3M EUR Libor **Estimation:** All variables in (log-)changes. All models include two lags of all variables and a constant. Responses and variance decomposition then estimated on residuals of these models. Inference based on a block-bootstrap algorithm (block size = 10) --- class: inverse, center, middle # 3. Empirical Results --- class: general # Impact of SNB Bill shocks .image-center-wide[  ] --- class: general # Impact of SNB Bill shocks .image-center-wide[  ] --- class: general # Impact of SNB Bill shocks .image-center-wide[  ] --- class: general # Impulse response functions (expectation shock) .image-center-narrow[ ] --- class: inverse, center, middle # 4. Concluding remarks --- class: general # Concluding remarks - Central bank debt securities can be used to tighten the policy stance without reducing the size of the balance sheet - Works even with large excess reserve balances, for a strictly positive yield on debt securities - Works through changing money demand rather than money supply - Important effects on financial market variables. Differences with respect to traditional monetary policy surprises + Effect on long-term rates is negative + Strong appreciation and decline in stock prices + Effect on expectations, even without central bank communication - Suggests that these new tools have side effects that do not directly work through money market rates --- class: inverse, center, middle # Thank you very much for your attention Do not hesitate to contact me if you have suggestions! **daniel.kaufmann@unine.ch** Canetg, F. and D. Kaufmann (2019), *Shocking Interest Rate Floors*, IRENE Working Paper 19-02, University of Neuchâtel Update available soon on **www.dankaufmann.com** --- class: inverse, center, middle # Appendix --- class: general # Interest on reserves > **Proposition 2:** *Suppose that commercial banks earn* `\(i_{ior}>0\)` *on reserves. If each commercial bank maximizes expected profits with respect to* `\(B_i\)` *and* `\(\pi_i\)`*, the money market rate equals* > `$$i_m^{ior}=i_{ior} + i_xP(X^{ior}>0)$$` - With ample reserves, `\(F\rightarrow \infty\)` and `\(P(X>0)\rightarrow 0\)`, thus `\(i_m^{ior}=i_{ior}\)` - IOR and debt securities are equivalent with ample reserves, that is, `\(i_{ior} = \pi i_b\)` --- class: general # SNB Bill yield vs. repo yield .image-center[  ] --- class: general # Repo bids and allotment .image-center[  ] --- class: general # SNB Bill volume and term to maturity .image-center[  ] --- class: general # SNB Bill yield vs. repo yield .image-center[  ] --- class: general # Reverse repo and SNB Bill marginal yield .image-center-narrow2[  ] --- class: general # Extensions - Estimate dynamic causal effects with local projections (Jorda, 2005). Requires stronger identifying assumptions + Estimate impact using the residuals (one-step-ahead forecast errors) + Estimate impact after `\(h\)` periods using the `\(h\)`-step-ahead forecast errors + Sign restriction on cumulative response - Estimate variance decompositions - Test the identifying assumptions, that there are indeed two independent SNB Bill shocks --- class: general # Impact of SNB Bill shocks .image-center-wide[  ] --- class: general # Placebo tests .image-center-wide[  ] --- class: general # Placebo tests - Treasury auction days - USD SNB Bill auctions - Payment days --- class: general # Robustness tests - Lag length (0, 4) - Block size (20) - Stock price indices (SPI, MSCI) - Point restrictions (Nakamura and Steinsson, 2018) - Bilateral exchange rates - Narrow definition of other events (ECB and SNB policy decisions) - Broad definition of other events (in addition, USD operations, treasury, government bond auctions, foreign exchange swaps)